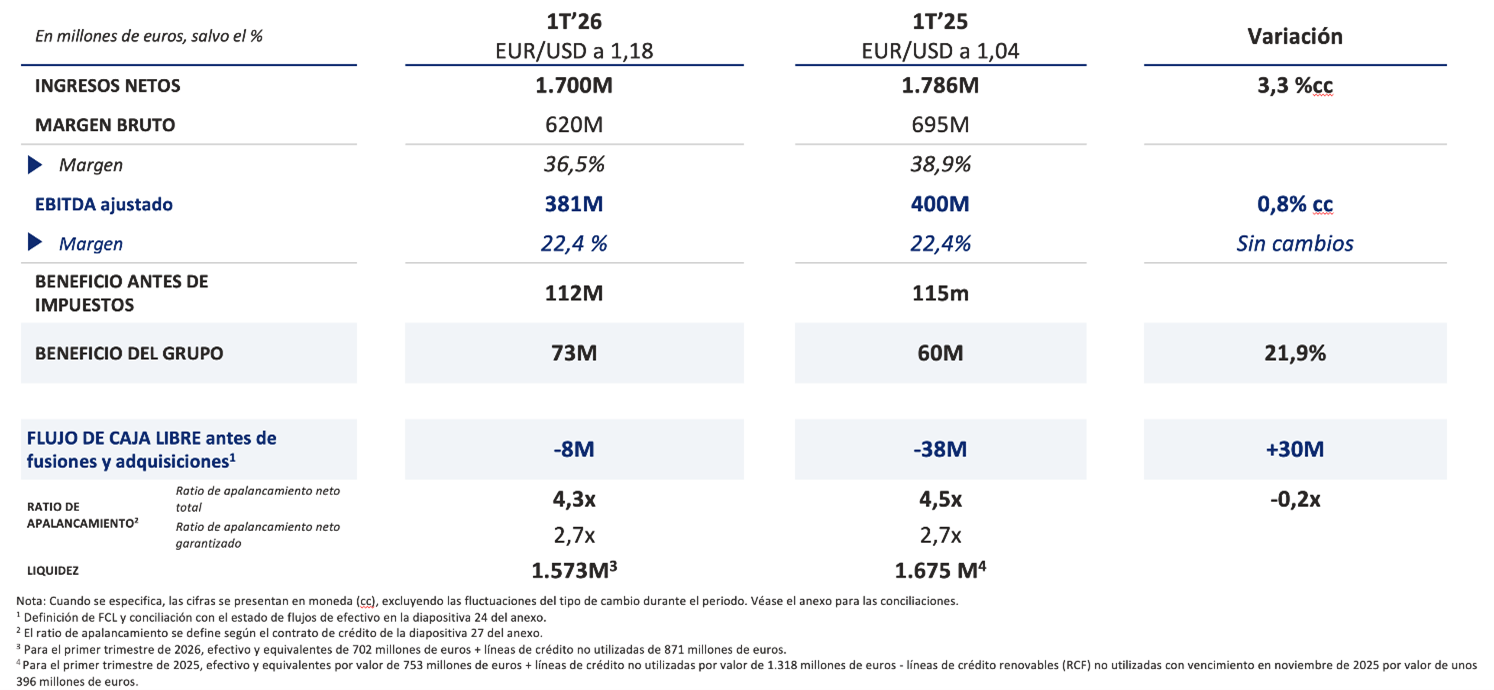

Barcelona, 7 de mayo de 2026 - Grifols (MCE:GRF, MCE:GRF.P, NASDAQ:GRFS), compañía global del sector de la salud y líder en la producción de medicamentos derivados del plasma, registró unos ingresos de 1.700 millones de euros en el primer trimestre de 2026, lo que representa un crecimiento interanual del 3,3% a tipo de cambio constante (cc), impulsado por el sólido desempeño de su negocio de Biopharma, que creció un 6,8% cc, liderado por la fortaleza de la franquicia de inmunoglobulinas (IG). En términos reportados, los resultados se vieron afectados negativamente por el impacto del tipo de cambio.

El crecimiento estuvo respaldado por el lanzamiento en EE. UU. de la IGIV de nueva generación de Biotest, Yimmugo®, así como por el desempeño sostenido de Gamunex® en EE. UU. y en los principales mercados europeos, que contribuyeron al impulso del trimestre. La evolución de los ingresos se vio parcialmente compensada por la presión de precios en albúmina en China y una base comparativa más exigente en alfa‑1 y proteínas especiales, reflejo de un ejercicio anterior que se benefició de aprovisionamientos extraordinarios de inventario tanto en alfa‑1 como en otras proteínas.

El EBITDA ajustado alcanzó los 381 millones de euros, con un crecimiento del 0,8% cc, y un margen estable del 22,4%, reflejando la disciplina operativa continuada en el conjunto de las actividades del grupo. El crecimiento del EBITDA estuvo respaldado por mejoras continuadas de eficiencia y una reducción del 7,7% cc de los gastos operativos, parcialmente compensadas por el impacto anualizado de las concesiones de precios de albúmina en China que afectan al primer semestre de 2026, así como por un impacto negativo por tipo de cambio de 23 millones de euros, derivado de un dólar estadounidense más débil.

Grifols prevé una mayor expansión de márgenes impulsada por la mejora del margen bruto, apoyada por el incremento progresivo del plasma de Egipto y las correspondientes ventas de inmunoglobulinas, la optimización continuada del aprovisionamiento y de la huella de plasma, así como por los crecientes beneficios en el coste por litro (CPL), junto con los avances continuados en la transformación operativa de Biotest y el apalancamiento operativo.

El beneficio neto del grupo aumentó hasta los 73 millones de euros en el primer trimestre, lo que supone un incremento interanual del 21,9%.

El flujo de caja libre antes de fusiones y adquisiciones del primer trimestre mejoró en 30 millones de euros interanual, hasta –8 millones de euros, respaldado por la gestión del capital circulante y la reducción del Capex y de los costes financieros. A cierre del 1T 2026, la ratio de apalancamiento se situó en 4,3x, mientras que la liquidez ascendió a 1.573 millones de euros.

Recientemente, Grifols refinanció con éxito todos los vencimientos de deuda de 2027, reforzando su flexibilidad financiera y el perfil de su balance. La refinanciación incluyó un Term Loan B ampliado de aproximadamente 3.000 millones de euros equivalentes y el incremento del compromiso de la línea de crédito revolving desde 938 millones de dólares hasta más de 2.000 millones de dólares, con condiciones de precio más favorables y mayores vencimientos, respaldado por una sólida demanda institucional y el apoyo de entidades financieras globales. Junto con la amortización parcial anticipada de 500 millones de euros del bono de mayor coste con vencimiento en 2030, estas actuaciones sitúan los intereses en efectivo de 2026 en línea o por debajo de los de 2025. Grifols no tiene vencimientos de deuda significativos hasta octubre de 2028 y mantiene una sólida posición de liquidez.

Durante los últimos 18 meses, las agencias de calificación crediticia han mejorado en varias ocasiones la calificación corporativa de Grifols. Standard & Poor’s (S&P) elevó el rating del emisor en dos escalones hasta ‘BB-’ con perspectiva ‘estable’. De igual modo, Moody’s y Fitch Ratings también mejoraron la calificación y/o la perspectiva de Grifols, destacando el fortalecimiento del perfil financiero de la compañía, la mejora de la senda de desapalancamiento y los avances continuados en la solidez del balance. Las tres agencias reconocen que Grifols cuenta con unos fundamentales de negocio equiparables a grado de inversión.

Nacho Abia, CEO de Grifols, ha dicho: “Empezamos el año con un desempeño en línea con nuestras expectativas y con la confianza de estar en posición de cumplir el guidance para el conjunto de 2026, a medida que seguimos ganando impulso a lo largo del ejercicio. Estos resultados se han logrado en un entorno geopolítico y macroeconómico complejo, marcado por la persistencia de incertidumbres, y ponen de manifiesto tanto la resiliencia de nuestro negocio como la solidez de nuestros fundamentos”.

Rahul Srinivasan, CFO de Grifols, ha añadido: “Seguimos avanzando de forma tangible en todo el negocio, apoyados por el fuerte impulso de nuestra franquicia principal de inmunoglobulinas. Asimismo, hemos logrado avances decisivos en el fortalecimiento de nuestra estructura de capital tras la exitosa refinanciación de este trimestre, lo que nos deja con una sólida liquidez, sin vencimientos relevantes hasta el cuarto trimestre de 2028 y con unos intereses en efectivo en 2026 en línea o por debajo de los de 2025”.

La próxima Junta General de Accionistas está previsto que apruebe el dividendo final en efectivo con cargo a 2025, reforzando el compromiso de Grifols con la creación de valor sostenible para el accionista. Esta decisión refleja la mayor flexibilidad financiera de la compañía y su foco continuo en una asignación disciplinada del capital, apoyada por los avances en el desapalancamiento y la mejora de la generación de flujo de caja libre.

Biopharma se mantiene como principal motor de crecimiento

Los ingresos de Biopharma aumentaron un 6,8% cc en el primer trimestre, reforzando el papel de esta unidad de negocio como principal motor de crecimiento del grupo. La franquicia de inmunoglobulinas (IG) creció un 15,3% cc, con la inmunoglobulina intravenosa (IGIV) aumentando un 16,2% cc, impulsada por la tracción sostenida de Gamunex en EE. UU. y en los principales mercados europeos, así como por el lanzamiento en EE. UU. de Yimmugo, que continúa reforzando el impulso de las marcas existentes de la compañía. La inmunoglobulina subcutánea creció un 5%, con un crecimiento continuo de doble dígito de la demanda en mercado de Xembify®, parcialmente compensado por la calendarización de inventarios.

La albúmina descendió un 6,1% cc, reflejando la presión continuada en precios impulsada por el gobierno en China, en línea con las dinámicas de mercado anticipadas a cierre de año que afectan al conjunto del sector sanitario en el país. Tras varios años de fuerte crecimiento, la demanda se estancó en 2025, lo que dio lugar a ajustes de precios a mitad de año. Con unos precios más estables en los trimestres recientes, la compañía mantiene una perspectiva constructiva para la albúmina en el conjunto del ejercicio. Grifols continúa apoyándose en su alianza estratégica local con SRAAS, combinando una política de precios disciplinada, una mayor huella comercial conjunta y un enfoque más preciso en contratación y marketing para incrementar la presencia en hospitales de menor dimensión y ampliar la presencia en farmacias. De forma paralela, la compañía sigue explorando oportunidades de crecimiento en mercados fuera de China, especialmente en EE. UU., para respaldar el equilibrio global del porfolio.

Alfa‑1 y las proteínas especiales descendieron un 7,4% en este primer trimestre de 2026, reflejando una base comparativa más exigente frente a 2025, ejercicio que se benefició de aprovisionamientos extraordinarios de inventario tras un cambio en el modelo de distribución. En alfa‑1, la base de pacientes continuó creciendo, lo que pone de manifiesto la persistencia de necesidades médicas no cubiertas. La compañía mantiene su foco en ampliar el diagnóstico y el tratamiento, mientras que la lectura prevista del estudio fase 3 SPARTA en el segundo semestre de 2026 representa un posible punto de inflexión relevante para la franquicia, al apoyar una mayor concienciación, un mejor acceso y la expansión del mercado a largo plazo.

Proyectos estratégicos que respaldan la expansión de márgenes a largo plazo y la optimización del suministro

Grifols continúa avanzando en iniciativas estratégicas clave para reforzar su modelo operativo a largo plazo y su rentabilidad. El proyecto de Egipto sigue avanzando conforme a lo previsto y se está convirtiendo en un elemento central de la estrategia de autosuficiencia de la compañía y de su plan de optimización del plasma a largo plazo. Más allá del aumento de capacidad, se espera que contribuya de forma estructural a la expansión de márgenes mediante una mejor alineación del aprovisionamiento de plasma con la economía de los mercados locales.

A medida que aumentan los volúmenes de plasma procedentes de Egipto, Grifols prevé optimizar progresivamente su huella global de plasma, reduciendo la proporción de plasma de origen estadounidense destinada a mercados fuera de EE. UU. y mejorando la economía global del plasma. La compañía prevé que la recogida de plasma en Egipto alcance aproximadamente 1 millón de litros en 2026 y hasta 3 millones de litros en 2029, lo que permitirá un reequilibrio gradual de la red global de plasma. Como resultado, Grifols espera reducir la dependencia del plasma de origen estadounidense para mercados fuera de EE. UU., mejorar la eficiencia de costes por litro y reforzar la resiliencia del suministro.

Tras la aprobación por parte de la Agencia Europea del Medicamento (EMA) de toda la cadena de valor de Grifols Egypt, la compañía se encuentra en una posición óptima para optimizar con mayor eficacia su red global de plasma, reduciendo progresivamente la dependencia del plasma de origen estadounidense para mercados fuera de EE. UU. Entre 2025 y 2029, se espera que el suministro de plasma fuera de EE. UU. aumente más del doble, impulsado en gran medida por Egipto. Se espera que este reequilibrio mejore la economía del plasma, respalde un crecimiento de medio a alto dígito simple del suministro fuera de EE. UU., refuerce la resiliencia del suministro y contribuya a un perfil de márgenes estructuralmente más sólido. Esta estrategia no solo permitirá a Grifols ampliar su huella industrial y de plasma, sino también redefinir la economía de aprovisionamiento y suministro global de terapias derivadas del plasma.

Asimismo, el reciente reconocimiento de las terapias derivadas del plasma como activos estratégicos en virtud de la Sección 232 de la Ley de Expansión Comercial de EE. UU. refuerza aún más la relevancia estructural del modelo verticalmente integrado de Grifols.

Desempeño de Diagnostic en línea con las expectativas

El desempeño del negocio de Diagnostic en el trimestre se vio afectado por la disolución anticipada del negocio conjunto con Quidel Ortho, que tuvo un impacto negativo puntual en los ingresos de las soluciones de diagnóstico por inmunoensayo (IDS). Este impacto se ve parcialmente mitigado por una compensación total de 65 millones de dólares que se recibirá entre 2026 y 2028. Excluyendo este efecto, el resto del negocio de Diagnostic tuvo un desempeño en línea con las expectativas, con un crecimiento de ingresos en términos comparables de bajo dígito simple.

Desde un punto de vista estratégico, la disolución del negocio conjunto otorga a Grifols un control total sobre su hoja de ruta en diagnóstico clínico, respaldando el desarrollo de sus plataformas de nueva generación. La compañía avanza en el lanzamiento de su plataforma de soluciones de tipaje sanguíneo, desarrollada en Barcelona, que incorpora tecnología de tarjetas de gel modulares y trazables y un flujo de trabajo simplificado, cuya presentación está prevista para el segundo trimestre de 2026. Este hito respalda la hoja de ruta global de innovación de Grifols en Diagnosis y su ambición a largo plazo de reforzar su posición en tipaje sanguíneo y cribado de donantes.

Guidance 2026

Grifols confirma que el desempeño del 1T 2026 estuvo alineado con las expectativas y respalda su guidance para el conjunto del ejercicio 2026.