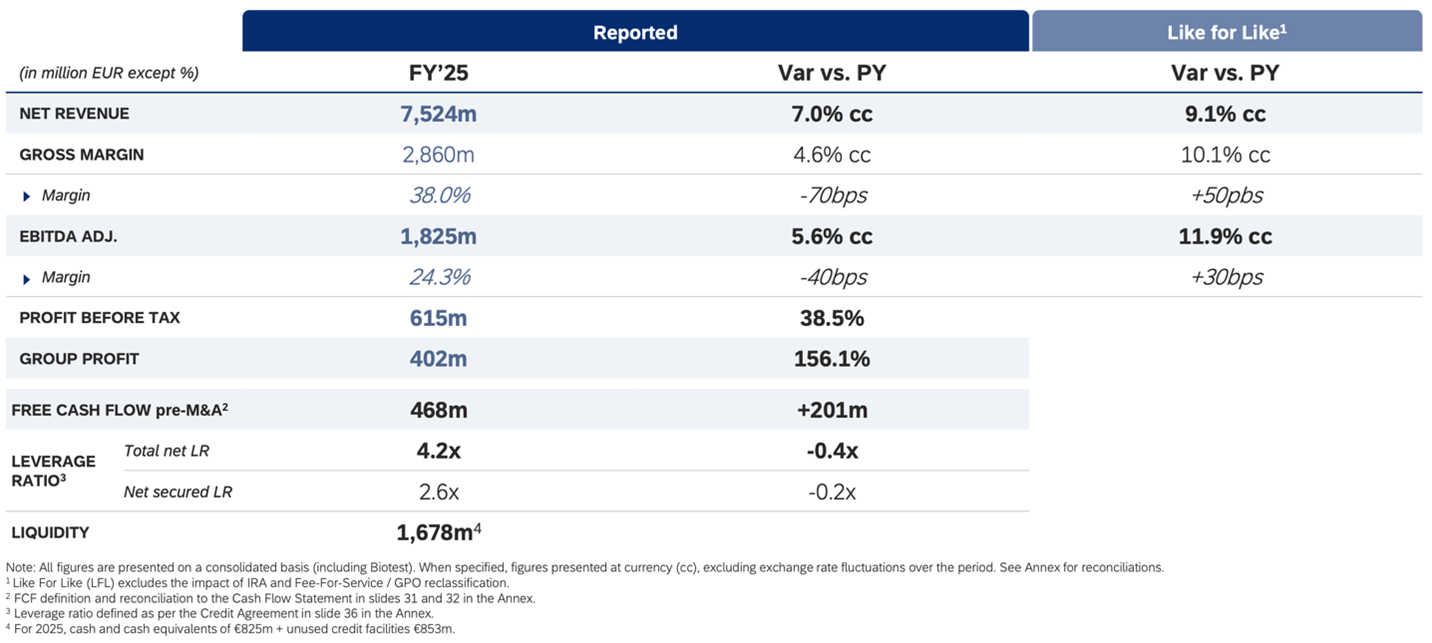

Barcelona, Spain, February 26, 2026 - Grifols (MCE:GRF, MCE:GRF.P, NASDAQ:GRFS), a global healthcare company and leading producer of plasma-derived medicines, reported a revenue of EUR 7,524 million in 2025, which represents a 7.0% cc growth, primarily driven by the continued strength of the Biopharma business, particularly the immunoglobulin franchise, as well as continuing to make progress on strategy and delivering the milestones of the Diagnostic business unit.

Adjusted EBITDA reached EUR 1,825 million, representing a 5.6% cc (+11.9% cc like-for-like) growth versus previous year, with a margin of 24.3% (25.0% like-for-like). Performance was driven by volume growth, continued cost per liter reduction and strict financial discipline.

Grifols more than doubled its net profit to EUR 402 million from EUR 157 million in 2024, a 156.1% increase, driven by higher operating margin and lower financial costs. Free cash flow pre-M&A amounted to EUR 468 million, representing a EUR 201 million improvement versus 2024. This performance was supported by EBITDA expansion, working capital management, lower interest costs and a normalizing level of capex after the 2024 high, together reflecting structural improvements in cash flow generation.

Grifols maintained its strong focus on balance sheet strengthening in 2025. The leverage ratio declined from 4.6x in 2024 to 4.2x in 2025, supported by improved EBITDA and robust free cash flow generation. The company currently expects to refinance its 2027 maturities in two steps – starting with RCF + TLB refinancing in the first half of 2026; followed by 2027 bond refinancing in Q4’26 or earlier.

Nacho Abia, CEO of Grifols, said: “2025 has been a year of successful execution in a complex environment. We have strengthened our key franchises, improved free cash flow generation and solidified our balance sheet with a deleverage focus, positioning the company to continue creating value for all our stakeholders."

Rahul Srinivasan, CFO of Grifols, added: “We are confident about Grifols’ highly differentiated strategy and positioning, which has been many years in the making and will support our continued margin improvement-led EBITDA growth, enhanced free cash flow generation and deleveraging path.”

Grifols financial and operational performance has been rewarded by strong re-rating progress across all three credit rating agencies: S&P upgraded Grifols’ credit rating to ‘BB-’ with a ‘Stable’ outlook; Fitch revised the outlook to ‘Positive’ and affirmed the ‘B+’ rating; Moody’s upgraded Grifols’ rating to ‘B1’ from ‘B2’ with a ‘Stable’ outlook. All three credit rating agencies acknowledge Grifols’ strong investment grade-like business characteristics.

Revenue performance led by Biopharma

Biopharma delivered an 8.4% cc (10.9% cc like-for-like) increase in 2025, reinforcing its role as the Group’s primary growth engine. Performance was driven by robust underlying demand across key markets, especially in the immunoglobulin (IG) franchise.

IG revenues increased 14.7% cc (17.7% cc like-for-like), outperforming the market and executing Grifols’ plan to gain share in the U.S. IVIG have continued to deliver double-digit growth, supported by the intravenous formulation, increasing 12.1% cc, while the subcutaneous formulation, XEMBIFY®, maintained strong momentum, rising 59.5% cc.

Albumin declined 5.1% cc (5.2% cc like-for-like), reflecting market and pricing dynamics in China. Pricing pressure in the country continues to be driven by government-imposed cost controls across the healthcare sector. The company continues to leverage its strategic local partnerships with Shanghai RAAS and Haier to actively manage market dynamics in China, the key market for albumin.

Alpha-1 and specialty proteins increased 1.4% cc (3.8% cc like-for-like), reflecting solid underlying demand. Leadership in alpha-1 remains intact, supported by disciplined execution and a differentiated development roadmap. SPARTA with results expected in H2’26, is positioned to further strengthen clinical differentiation, expand awareness and accelerate growth, while SC 15%, targeted for 2028/2029, represents a meaningful lifecycle innovation opportunity. Together, these initiatives underpin the strategy to expand the total addressable market, enhance outcomes data and reinforce long-term category leadership.

Innovation: Launch of fibrinogen

Grifols has initiated the European launch of PRUFIBRY® in Germany, prioritizing markets where the transition toward fibrinogen concentrates is most advanced. From this, the company plans to expand into additional European markets over time, in line with local reimbursement pathways and clinical adoption.

In the United States, following FDA approval of FESILTY™ for congenital fibrinogen deficiency in December, Grifols is focused on establishing an early commercial presence, securing hospital formulary access, and building long-term relationships with key stakeholders.

Vertical integration in the U.S. and strategic self-sufficiency projects provide strong structural foundation for long-term value creation

The strategic investments of Grifols over many years provide the company with a strong structural foundation for its long-term value creation. This is particularly important in an environment where geopolitical pressures are rising, and supply security is becoming increasingly strategic for customers.

In the U.S. –the world’s largest IgG market– Grifols has over the last decades built a unique fully integrated, end-to-end platform spanning domestic plasma collection, fractionation, purification, and commercialization. Today, this platform provides meaningful structural advantages: supply security at scale, optimized plasma economics, operating leverage, and the flexibility to dynamically allocate supply in response to global demand and geopolitical shifts.

Over the last years, Grifols has started to extend this vertically integrated business model into other strategic markets through long-term public-private partnerships that align its capabilities with national healthcare priorities.

In Canada –the fourth-largest global IgG market– Grifols’ long-term partnership with Canadian Blood Services (CBS) supports the country’s objective of reaching at least 50% IgG self-sufficiency over time. By expanding the share of locally sourced plasma and adding the capabilities to convert it into domestically manufactured plasma-derived proteins, strengthening supply resilience while reinforcing its presence in an attractive market.

In Egypt, Grifols has partnered with the Egyptian government to establish a fully integrated plasma platform designed to achieve national self-sufficiency and position the country as a regional hub for Africa and the Middle East. Once domestic needs are fulfilled, this platform expands access to life-saving therapies across the region and creates export potential to European countries, especially for IgG.

Spotlight Egypt: Transforming national self-sufficiency into a regional hub powered by a new benchmark-quality plasma platform

In 2025, Egypt achieved 100% self-sufficiency in key proteins thanks to Grifols, becoming only the 6th country to do so worldwide. Grifols Egypt for Plasma Derivatives (GEPD) has established a fully integrated local ecosystem covering plasma collection, fractionation and manufacturing, backed by a EUR 280 million investment and designed to create a new sovereign plasma industry for the EMEA region. Throughout 2025, GEPD reached key milestones across construction, technology, regulatory and operational areas, including regulatory certification by the European Medicines Agency (EMA) of the full value chain.

The latter milestone establishes Egypt as the first fully integrated, EMA-certified end-to-end plasma ecosystem in Africa and the Middle East, positioning the country as a strategic regional platform capable of stimulating a high-value biopharmaceutical industry with strong export potential. Additionally, at a time when approximately 40% of Europe’s plasma supply is sourced from the United States, the platform contributes to greater supply diversification and supports enhanced strategic autonomy for European healthcare systems under the EMA certification. The platform is therefore positioned to convert surplus plasma into high-quality medicines across the EMEA region, contributing to structural margin resilience and long-term profitability through global protein optimization and value-added exports.

In 2026, the company will focus on executing the next industrial phase of this platform, with the objective of scaling volumes and consolidating local operations. The company will add four new donation centres, to reach a network of 20 centres by 2026, and will inaugurate Phase I of the new manufacturing facility including an automated testing laboratory and a dedicated plasma logistics centre. This marks the transition from infrastructure build-out to industrial scale-up.

2026 Guidance

In 2026, Grifols will prioritize margin-led EBITDA growth, continue free cash flow expansion and deleveraging progress, building on Grifols’ unique position in the industry, including self-sufficiency platforms in Egypt and Canada.

For 2026, Grifols expects reaching Free Cash Flow pre-M&A pre-dividends of EUR 500m-575m, an Adjusted EBITDA margin of ≥25% with continued Adjusted EBITDA growth of 5-9% at constant currency, and a continued deleveraging path. 2027 milestones are unchanged: credit agreement leverage of 3.5x or lower by year-end 2027 and cumulative FCF pre-M&A pre-dividends (2024-2027) of EUR 1.75-2.0bn.

1 Financial guidance refers to the guidance at guidance FX rate (EUR USD @ 1.04) provided at the Capital Markets Day (CMD) presentation (slide 38).

2 Operating or constant currency (cc) excludes exchange rate variations reported in the period.

3 Like For Like (LFL) excludes the impact of Inflation Reduction Act (IRA) and Fee-For-Service / GPO reclassification.

4 Calculated as Adjusted EBITDA +/-Changes in Working Capital - CAPEX (see reconciliation in slide 43 of the FY 2025 Results presentation) – R&D and IT +/- Others - Interest - Taxes. In the Consolidated Annual Accounts, this reconciles to Cash flow generation from operating and investing activities excluding impact from M&A and associated costs and expenses.

5 Leverage ratio defined as per the Credit Agreement in slide 36 FY 2025 Results of the presentation.